|

|

| themanager.org | Search |

Survey on the Growth Perspectives of the European Automotive Supplier Industry

- How Suppliers can win more Business in Europe -

November 2002

By Hanns Guenther Bollig

The Society of Motor Manufacturers and Traders (SMMT) commissioned Automotive Advisors & Associates to conduct a survey amongst the European automotive manufacturers and their largest first-tier suppliers about the growth prospects of the European automotive supply industry and the priority actions for suppliers and governments.

The report is based upon the six key questions:

1. In which areas will there be more outsourcing - in terms of value added?

2. What are the most pressing problems to be solved with the help of the suppliers?

3. Which areas require urgent attention by suppliers?

4. Which supplier groups are likely to gain more business?

5. What should be the priority actions for suppliers from the various countries?

6. What should governments do in order to draw more automotive business into their countries?

Respondents have been vehicle original equipment manufacturers (OEMs) and first-tier suppliers from Germany, France, Italy, Sweden, Austria and from the US.

In order to highlight the relevance of the findings for automotive suppliers, Automotive Advisors & Associates have analysed the development of the European automotive industry during the previous four years, and set the UK supply sector in context.

Development of the European automotive industry during the previous four years

The automotive industry in Europe has continued to grow over the last four years. However, business development has been very uneven and some countries have fared better than others. In the UK there has been growth in the manufacture and assembly of vehicles, but UK Office of National Statistics (ONS) data shows that there has seen a significant reduction in the number of component companies operating in the sector. SMMT data suggests that there are around 2000 companies whose main business is automotive component manufacturing sustaining 200,000 jobs and with a turnover of around £15billion in.

The automotive supply chain remains a key aspect of the UK economy, with 17 of the top 20 European supply companies operating in the country. These companies support the eight major global car manufacturers and nine commercial vehicle production facilities that operate in this market.

60 per cent of the vehicles produced in the UK are exported to European markets, with a wide range of products crossing all sectors. This breadth does provide great opportunities for suppliers.

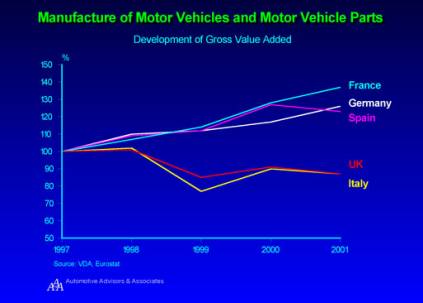

A key indicator for the sector shows that whilst the French, German and Spanish automotive supply industries have continued to grow, the supply industry in the UK may well have lost almost 20% of its business. This, despite the fact that a recent KPMG report demonstrated that the UK provides the second lowest cost base for the sector, compared to North America and Japan. Clearly cost alone is not the key issue in the automotive supply chain.

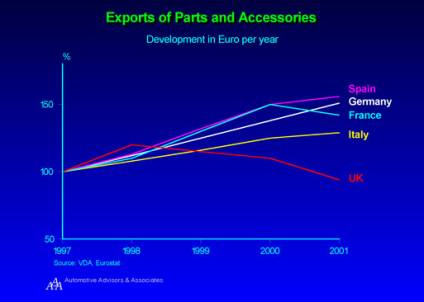

Interestingly, exports of parts and accessories have grown stronger in the more successful countries than the overall value added in their motor industries. This indicates the growing importance of international trade and exports in the European motor industry.

A particular example is Italy, whose automotive companies have been especially successful in partially compensating the downturn in their home market by increasing their exports. Without increasing exports, the Italian parts and accessories industry would have experienced an even sharper downturn. A similar picture can be observed in Spain, where a strong downturn in gross value added has been partially compensated by a slower fall in exports and therefore a greater stability in employment in the industry.

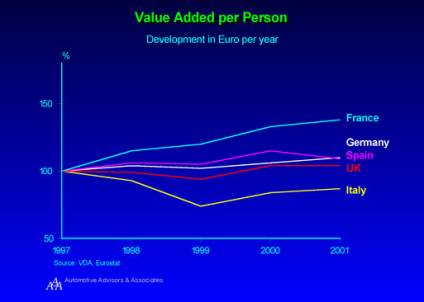

Part of this stability has been achieved at the expense of productivity (see graph “Value Added per Person”, next page).

Although low-cost performance and productivity growth are essential for maintaining competitiveness, it is apparent that there are additional factors that determine success in the automotive industry.

In order to survive and prosper with the challenge of this competitive environment, suppliers will have to understand the future structure of the market; the most promising areas for additional business and the factors that will make them win the fight against competition.

The results of the survey

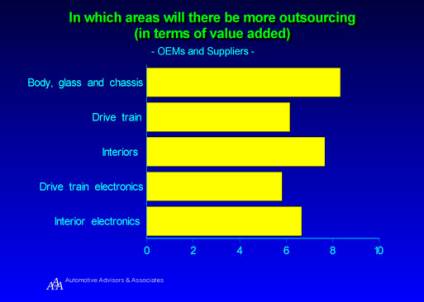

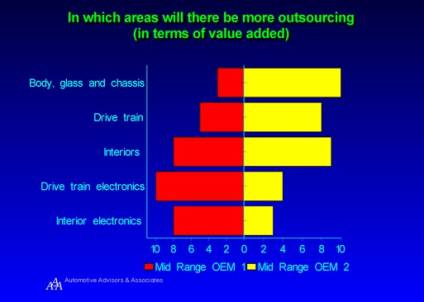

1. In which areas will there be more outsourcing by the vehicle manufacturers - in terms of value added?

The greatest opportunities for suppliers are the ongoing disinvestments of the vehicle manufacturers (OEMs). In order to make more funds available for product development, marketing and globalisation, they systematically seek to farm out more of the value added processes of production and engineering to their suppliers.

Across the industry, carbodies, glass, chassis and interiors are the first candidates for additional outsourcing of the OEMs. Hardly any vehicle manufacturer will invest in stampings and pressings in the future. Existing stamping and pressing plants are increasingly sold to suppliers and any production growth areas are likely to be farmed out. Seats and interiors will also remain strong outsourcing areas.

It is likely that any growth will go to the few mega suppliers that already dominate this sector. Smaller suppliers may well move from first tier to second tier level, and might have to find new niches with which they can provide service for the first-tier groups. This will entail a greater level of international marketing, co-development and further concentration on their core competencies for them.

The biggest challenge will be for the smaller ‘Jack of all Trades’ companies without specialised skills – and several respondents to the survey predicted that they may be unlikely to survive.

The OEMs, however, do not provide a uniform picture.

Different vehicle manufacturers are setting different priorities. Their individual outsourcing activities depend on factors such as their growth expectation, past achievements, current plant structures, unions, core competencies, product strategies and target markets.

It is essential for first-tier suppliers to identify the opportunities across the borders and with each individual vehicle manufacturer in Europe.

Outsourcing of body modules, glass and chassis parts are increasingly connected with outsourcing of car interiors. Both activities require a wide range of product capabilities and strong integration skills. However, outsourcing in drive train parts and components remains a highly specialised matter. Here again, the outsourcing strategies of the individual vehicle manufacturers are a reflection of their core strengths and weaknesses.

In many cases, the most advanced supplier groups are driving the technological innovation. These are the areas in which OEMs may decide to rely on the know-how of these supplier groups rather than developing their own.

2. What are the most pressing problems that should be solved with the help of the suppliers?

Cost and weight reduction have been, and will remain, the prime targets for the automotive industry in Europe. While cost reduction is a consequence of increasing competition and global markets, the goal of weight reduction has partially been imposed on OEMs by lower fleet consumption targets. However, competition has also triggered an ever-increasing number of accessories and vehicle electronics. Their additional weight has been the impetus for lowering the weight of the standard body and drive train components. The increasing number of new model releases and the need for faster technical innovation has revealed a number of weaknesses in the industry that have to be overcome. The survey identified these to be the most:

· ‘Right First Time’ - First class component quality and production readiness right from the start of a new model,

· Rapid technical innovation

· Systems integration

· Development of advanced on-board electronics networks.

Callbacks and delayed product launches are now causing serious problems for the automotive industry. OEMs are pressing their suppliers hard to improve performance and to create zero-defect supplies on time right from the start.

Whilst supply-readiness is primarily a matter of organisation and communication, systems integration and electronics networks are a matter of rapid research and development in high technology areas.

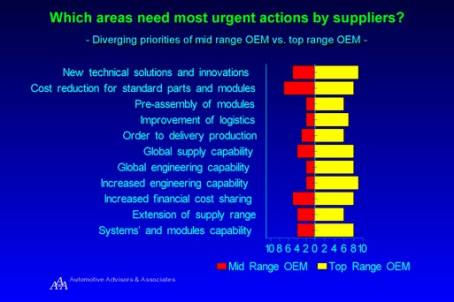

3. Which areas require urgent attention by suppliers?

Most vehicle manufacturers put cost reduction on top of their list of priority actions, closely followed by ‘new technical solutions and innovations’. The next most important issues on their wish list are an increasingly global supply capability by their suppliers and an improvement in logistics. This wish list indicates that the competitive pressure remains high.

Winning market share and improving sales short-term are currently more important than other measures that may be equally important, but take longer to achieve. On the other hand, suppliers whom they trust are few. This is the reason why OEMs value global supply capabilities and excellent logistics so highly.

However, the picture is not uniform. OEMs set different priorities for winning business and these can be split into two categories; top-range OEMs and mid-range OEMs.

The typical top-range OEM focuses on technical innovation, increased engineering by suppliers and improvements in their systems and modules capability even more than on simple cost reduction. They try to escape the cost squeeze by raising the perceived value of their vehicles above the actual costs and by creating new demand through rapid innovation.

Not all OEMs of course are in that league. Instead, some put cost-reduction first and seek suppliers that are willing and capable to share the costs. They focus on low cost suppliers and as a consequence ask them to manage a wider range of supplies globally; this improves their product scope by providing whole systems and modules. By setting these priorities, OEMs are trying to extend their low-cost parts supplies without entering the risk of lowering product quality by changing to new and unproven suppliers. The quality shock of the 80’s when global cheap sourcing was at its heights has left its traces.

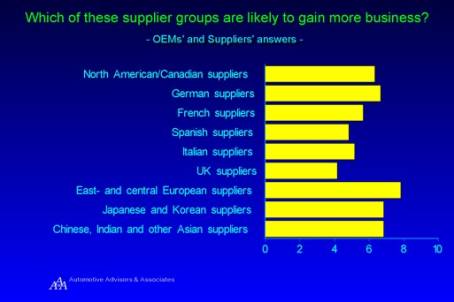

4. Which supplier groups are likely to gain more business?

The majority of the respondents said that suppliers from different countries have a different industrial focus and therefore perform differently. As a consequence, they believe that some countries will be more successful in winning new business than others.

As a whole, the European automotive industry looks East. OEMs put great efforts into seeking more supplies from Eastern and Central Europe, Japan, Korea, China, India and other Asian countries. However, despite the general trend to looking east, Germany’s suppliers are expected to win more new business than any other European country.

Almost equally strong will be the position of the North American and the Canadian automotive suppliers, which operate in Europe. Apparently, OEMs expect that these groups perform better and will help them reach their objectives faster.

French and Italian suppliers are expected to cover the middle ground. French suppliers in particular are trusted for its proven track record of productivity growth and quality.

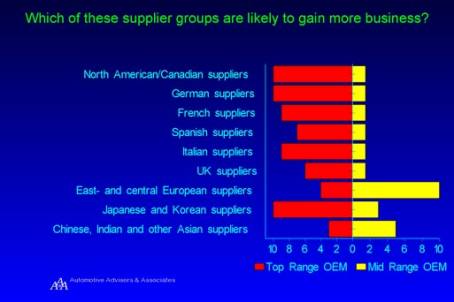

Why is this so and who prefers whom as

suppliers? The picture becomes clearer when the intentions and expectations of

two types of vehicle manufacturers are compared with each other, the typical

top-range OEM and the typical mid-range OEM.

The top-range OEMs, which focus on technical innovation, first-class engineering and strong systems and modules capabilities clearly favour the North American, German, French, Italian and Japanese suppliers. Apparently, the Spanish and UK suppliers are falling behind, partly because of perceived weak performance in innovation, engineering and other factors that are important to them.

Mid-range OEMs on the other hand are turning away from their traditional European sources. The structural costs of labour in these countries are too high. Instead they are seeking new low-cost suppliers in Eastern and Central Europe, Japan, Korea, China, India and other Asian countries.

Three factors may play a dominant role in this decision:

· Cost considerations outweigh technological innovation and engineering capabilities by far

· OEMs, which produce cars or components in Poland, the Czech Republic, Hungary, China and India have been highly successful in training local sources with the help and supervision by their Western suppliers. They trust that if they can supply them well in their home country, they should be able to do the same in Europe.

· OEMs, which have acquired shares in other Japanese and Korean OEMs have discovered the Korean and Japanese supplier base. Through their acquisitions, cultural barriers have been overcome and common development links have been established.

Cost pressure and the diverging escape strategies of the European OEMs may well split the European supplier market. Highly innovative suppliers with strong systems and engineering background could well continue to grow in partnership with their customers.

Squeezed in the middle are those, which have failed to invest sufficiently in innovations and new systems technologies. They will have to decide to either follow the innovation trail or to beat the East on the basis of costs. Staying undecidedly in between may lead to further decline.

5. What should be the priority actions for suppliers from the various countries?

The actions that vehicle manufacturers (OEMs) suggest for the suppliers from the various countries are a result of perceived weaknesses and needs for improvement:

· The US needs further cost reduction and better logistics

· Germany needs strong cost reduction and more engineering capacity

· France should expand its global outlook in supplies as well as in engineering

· Spain and Italy need stronger globalisation of supplies and of engineering and more innovations

· The UK suppliers are asked to be more innovative, acquire a broader capability in systems and modules and be willing to offer more pre-assembly operations for the

· OEMs

· East and Central Europe need to acquire a broader systems and modules capability and to extend their capabilities beyond Europe

· Japan and Korea should improve their global supply capabilities, increase their international engineering staff and improve their logistics capability globally.

· Chinese, Indian and other Asian suppliers need to do the same. In addition, they must improve their production to order capability significantly.

6. What should governments do in order to draw more automotive business into their countries?

OEMs and suppliers alike believe that the foremost objective of any government should be to let business do what business does best: doing business. Governments should not interfere with international trade nor create barriers nor provide subsidies. Instead, they should create a positive enabling environment by lowering taxes, eliminating the risks of currency fluctuations and increase training, labour skills and research capabilities in their countries.

Requests in detail:

· Enable competitive cost structures (taxes, labour, currency parities)

· Enable trade without barriers, taxes or subsidies

· Create attractive tax incentives and cut taxes generally

· Reduce bureaucracy in international trade

· Increase incentives for R&D

· Provide greater financial incentives for setting up or extending plants

· Improve training and labour skills

This report is also available as an e-book in PDF format. Please contact

hanns.g.bollig@automotive-advisors.com (Please state your company and function)

If you want to know more, please contact us: Automotive Advisors & Associates