|

|

| themanager.org | Search |

The Internet: Redefining relationships in the supply chain

By Hanns Günther Bollig ©

Nick Scheele, President of Ford of Europe: "Introducing the Internet is not just a change in technology. It will initiate the biggest cultural change the automotive industry has seen in a century".

When talking to automotive executives today, one may find that the views regarding the impact of the Internet on the automotive industry are not at all uniform The reason for this is the fact, that the Internet is only a facilitator of strategies, not a strategy in itself. These strategies are only emerging as the opportunities provided by the Internet become clearer.

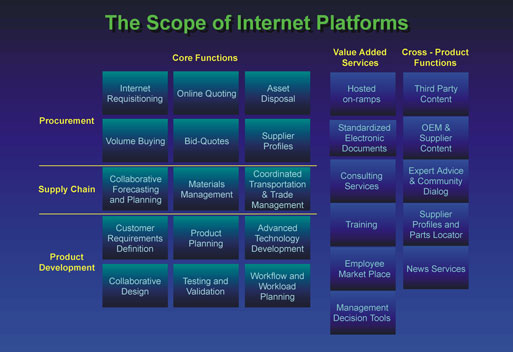

Graph 1

The scope of the Internet platforms is vast as this table of COVISINT-functions shows (Graph1). It provides means for nearly everything one can think of in the process of making a car. But there is more to it than that. Nick Scheele, President of Ford of Europe, is of the opinion, that introducing the Internet is not just a change in technology. It will initiate the biggest cultural change, the automotive industry has seen in a century.

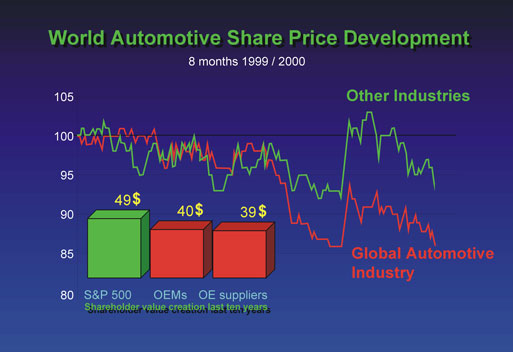

Graph 2

Over the last couple of years, the automotive industry has lost much of its appeal to financial investors (Graph2). Share prices have been decreasing constantly. Worse than that, shareholder value creation has been twenty per cent lower than the industry average. Profits are continuing to decline. In an expanding, capital hungry industry, this developing is devastating. Is the automotive industry in the typical position of any other "old economy" where manufacturing is becoming increasingly unattractive and profits can only be achieved by diversification into other businesses? The automotive industry is determined to turn its fate. It is apparent, that the obvious is done first. Reports about the success of negative price auctions, consolidation of group purchases, reduction of administrative costs and the beginning of direct sales over the Internet have filled the news. However, the historic underperformance in shareholder value creation shows that cost reduction alone will not be sufficient. The automotive industry has therefore set out to exploit their most valuable asset, the customer base. The next generation of Internet applications will therefore set out to achieve this.

Graph 3

If the vehicle manufacturers could establish and keep direct contact with their new car buyers, the automotive industry could gain access to more than 250 Million customers globally (Graph3). If the second hand car market could be equally controlled by the OEMs, this number would increase to more than 500 Million customers worldwide. This would be the largest and highest valued customer base of any industry. Of course, keeping contact with the customer over the whole period of ownership is difficult, if it only concerns one new car purchase every seven years. Contacts must be refreshed more frequently. Other products and services must be found to bridge that gap. We already see a number of such related product sales increasing rapidly. Telemetric services, insurances, finance products, car rentals, lifestyle products, events and any other product range which could be associated with the brand. Another growing field of intermediate sales will be the whole range of vehicle specific consumer electronics. With a renewal rate of two years, such electronic equipment could be sold six to seven times during the full live cycle of an average car. As these products could reach a value of near 30% of the value of the car, total life cycle sales could be more than twice the value of the car.

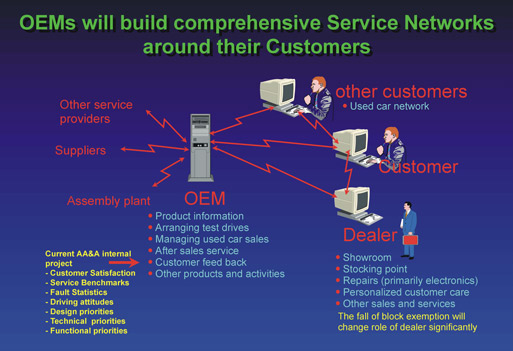

Graph 4

Unfortunately for the OEMs, the dealers hold access to the customer base. Lifting block exemption in Europe will enhance this problem. OEMs will therefore seek to reduce the role of the dealerships rapidly. The Internet is the given means for doing that. Prospects for selling cars via the Internet are good. A recent pan European survey showed that 25% of all car purchases are already carried out without a prior visit to a dealer's show room. These purchases could almost certainly be executed via the Internet without any delay. It is no surprise that Mercedes had the largest portion of such "blind sales". Apparently the image, prior experience and sheer trust in the brand make it easier for customers to carry out such purchases. The future potential of Internet purchases is likely to be in the range of 60%. Only 40% of the surveyed Europeans claimed that they could not imagine buying a car without visiting a dealer first.

Selling cars via the Internet is not a unidirectional exercise. Equally important are other services like taking and selling used cars. More than 85% of all surveyed persons mentioned that the possibility and the price of traded in cars are major factors in their purchasing decision. OEMs must therefore develop a whole range of services alongside new car sales and should not leave this to the independent operators (Graph 4). The OEMs will include product information, arrange test drives, buy and sell used cars, provide after sales services, run customer feedback programmes and sell a wide range of other products in addition to automobiles via the Internet. In this range of services, customer feedback programmes will play an essential role. Not only is it possible to gather historic benchmarks and customer satisfaction data but the OEMs will soon be able to run car clinics via the Internet. They will also test customer perception of new technologies and conduct complete product and technology development round tables via the Internet. Automotive Advisors & Associates are currently carrying out an internal development programme, which will allow such safe exchanges of data and opinions. Whilst OEMs will control nearly everything around new and used car sales, the dealers will be left with showroom activities, local marketing, personalised customer care programmes, stocking point, car deliveries and other direct customer related services.

Whilst the "hard values" will be nearly common for all vehicles and all brands, the "soft values" will dominate the agenda. Individuality, lifestyle, environment, customer care, mobility packages, availability and supply lead time of cars. The latter factors: availability and supply lead time will have a decisive impact on the way cars will be built and sold into the market place.

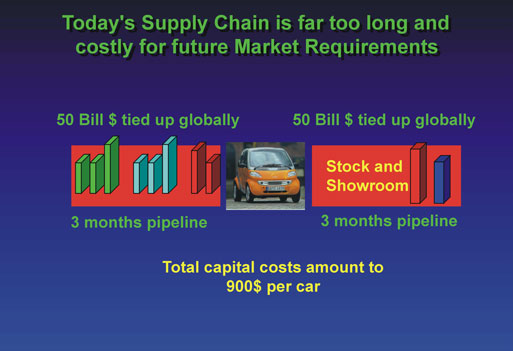

Graph 5

Today's supply chains are far too long and costly for future market requirements (Graph 5). Globally, more than $100 Billion are tied up in a six months long supply chain. These costs amounts to more than $900 per car. A sum, far too high. Traditionally, action plans are targeted at reducing inventories. With the Internet, attention will have to concentrate on another issue: the shortening of the supply chain. By doing so, inventories will decrease automatically whilst customer service is increased.

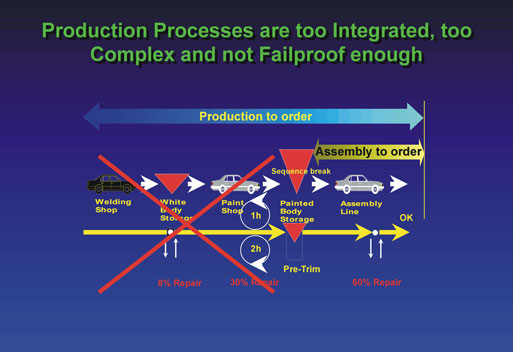

Graph6

One reason for the problem of long lead-times and high costs is the fact that production processes are far too integrated, too complex and too prone to failures (Graph 6). In the attempt to keep costs down, the industry has believed that integrating and timing as many processes down the supply chain as possible would do the trick. This is not the case. Already in the very short production processes applied in a car plant, the faults occurring whilst building and painting the body in white causes serious disruption of the whole process. Unfortunately, these faults cannot be corrected quickly enough so that sequence changes occur in a magnitude, big enough to disrupt the whole supply plan. In the automotive industry, throughout the whole supply chain, these and other disruptions are the reason that nearly 60% of all daily production plans are changed the same day they were set up. The concept of "producing to order" needs therefore to be complemented by the concept of "assembling" to order. What will the Internet do to improve this? Building cars is not a parallel process. It is largely sequential. Imagine you watch a group of soldiers marching by. The soldiers represent the supply chain. The band represents the market. You may recognise that keeping the soldiers marching to the same stroke will become increasingly difficult, the longer the line of soldiers is. The soldiers in the rear may step out of stroke, because the music doesn't carry that far, or one of the soldiers in the middle stumbles, causing the others behind him to fall. Someone wanting to cross the road may also recognise that waiting until all soldiers have marched by, can take too long. Translating this picture into supply chain language: The Internet will carry the music to everyone. So everyone in the chain could march to the same tune. This will help keeping the "soldiers" in stroke. However, the Internet will not prevent a soldier from stumbling or the chain being too long for the customer to cross the road (receive his custom produced car).

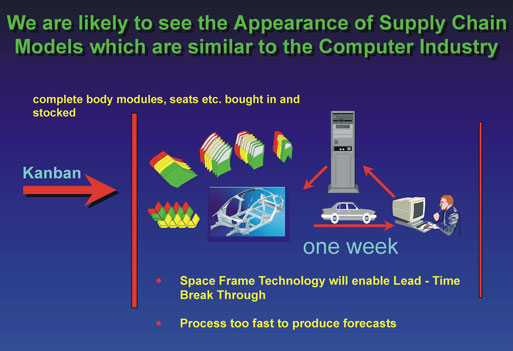

Graph 7

We are likely to see the appearance of supply chain models, which are similar to the computer industry (Graph 7). Technology must help. Nearly 80% of the OEMs see the space frame technology being the technology of the future for all vehicles below 100,000 to 150.000 production units per year. This technology could therefore cover the wide range of niche models targeted at promoting the brand and serving the ever-increasing number of individuals, seeking to express themselves through their cars. Within three to four years, the problems of colour matching are likely to be solved. Integrated body modules will be supplied. Assembly to order within one week could be achieved. However, this assembly to order process will be too fast for issuing forecasts to suppliers. As the example of the truck industry is already showing, OEMs may drop their forecasts and each supplier may have to produce to his own stock. Traditional MRP Systems will become obsolete for every production to order vehicle. However, production to plan will still be around, but the market will be strongly segmented, very similar to the consumer goods industry (Graph 8):

Graph 8

The "Cash & Carry" market: The take-away vehicle characterizes this market: built to stock for immediate pick up by the customer. This segment comprises the low-cost, high volume vehicle for the mass market. Sold through various channels including free dealerships and supermarkets. More than today, this market will be governed by a repetitive series of push-activities, special action models and high rebates. The marketing department of the OEM will push the supply chain, with short but precisely phased supplier lead-times and pre-determined production lots. Whilst the supply chain will work to a firm production order, the great flexibility will lie on the distribution side.

The "sophisticated pull-market": The built to order vehicle will dominate this segment. High volume upper market vehicles, which command prestige and distinction and for which the customer is willing to wait. Customer order lead-time could be up to four weeks without losing sales to other brands. There will be an ordering pipeline for the suppliers, which could see the incoming customer orders filling the capacity slots day by day. The base for a third, second and first tier supply chain moving in stroke with the OEMs in producing this made to order car.

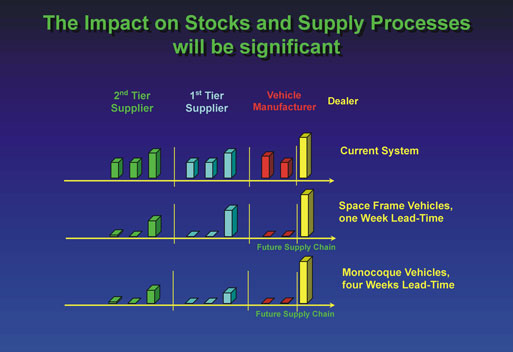

Graph 9

The "sophisticated push-pull" market: The assembled to order vehicle will be the dominant player in this market. It is characterized by rapid response to customer order, following some element of impulse buying by the customer. Space frame technology is likely to be the dominant technology. Suppliers will produce highly integrated modules to stock. One-week customer-order lead time could become standard. A mixed push-pull market approach could be used to maximise sales.

Graph 10

Graph 11

Not all OEMs may serve all three markets. The mentalities, the production concepts and the distribution systems may be too different to find a home under one roof. Different brands, dedicated production units and different dealer groups may be formed. With the fall of the block exemption, more OEMs will strive to own a captive dealer network. Customers may also become more flexible. They may either chose to travel over some distance to pick up the cheapest car of their choice or to visit one of the showrooms of the brand they prefer. As a consequence, showroom activities may be more concentrated and increasingly separated from the repair and service units as compared to today.

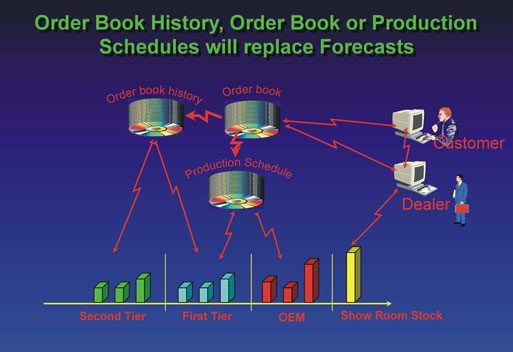

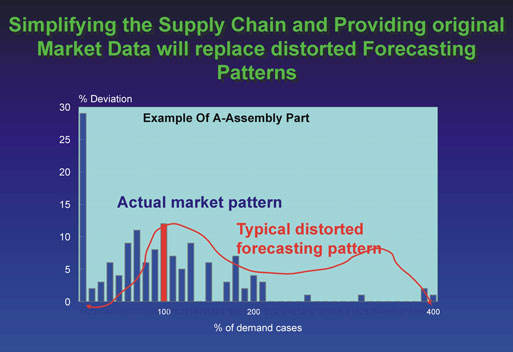

Depending on the segment, order book, order book history or firm production schedules will replace forecasts (Graph 9). Firm production schedules and order book for all suppliers, which are able to produce within the given lead-time, order book history for everyone else. Each of the market segments will play to their own rules. Industries, which have traditionally operated in such segmented markets, found that operating different systems at the same plant interfere with each other. Dedicated plants are likely to emerge. Giving suppliers access to original market demand data, broken down by part or component, would be a major instrument for reducing inventory and reducing lead-time (Graph 10). Comparisons between original market demand patterns, broken down by parts and components showed that these demand pattern are more regular than the distorted demand pattern created through the influence of today's planning processes. Based on these analyses, we believe that inventories in the supply chain could be almost halved (Graph11). The impact on stocks and supply processes will be significant. Typical patterns of the distribution of inventories over the supply chain - before and after using the Internet - are shown in this graph. The Internet breaches regional barriers. Supply chains can be extended without generating high penalty costs. Some OEMs believe that supplier parks may become redundant or shrink. Producing at the lowest cost location is likely to become more important than producing at the most flexible location near an OEM. Whilst branding will be a major issue for the OEMs, large suppliers may follow suit.

This article was provided by courtesy of Mr. Hanns Günther Bollig,

Automotive Advisors & Associates