|

|

| themanager.org | Search | German Portal | Bookstore |

|

|

Findings indicate that co-movements among the U.S., Germany, and Japan markets are significant. Burhan F. Yavas, PhD

Graziadio Business Report,

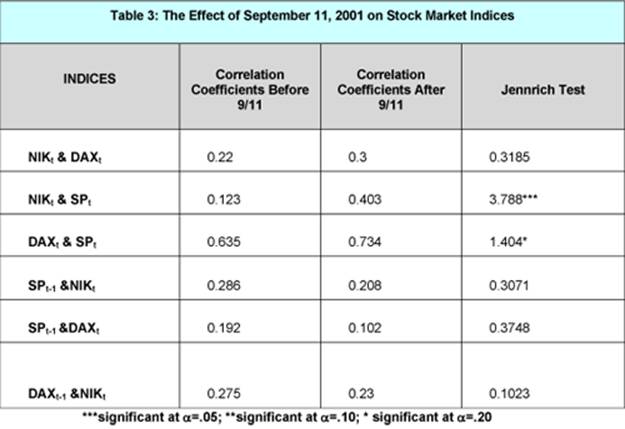

2007, Vol. 10, Issue 2 Stability of Interdependencies among Markets Finally, we utilize event methodology to test the hypothesis that correlations among markets are significantly higher following exogenous events. Longin and Solnik and Karolyi and Stulz[7] are examples of two of the studies that find that the correlations between the major stock markets increase after global shocks. To see if data used in this study could provide support for the above hypothesis, we studied the September 11, 2001, terrorist attacks on the World Trade Center in New York, the Pentagon in Washington, D.C., and on a plane that crashed in a field in Pennsylvania. The 9/11 event is important event to study because the most powerful country in the world was targeted on its own soil on such a scale that these events shook confidence throughout the entire global economic system. Following the attack, major world stock market indices declined and trading was halted in the U.S. To investigate the effect of the 9/11 attacks on the stability of the interdependence of the markets, we conducted tests that addressed the question of whether the correlations would remain constant over the adjacent sub-periods. It is recommended that the sample period before the event should exceed the sample period after the event.[8] Accordingly, we have chosen sample sizes of six months before and three months after the September 11 event. The findings reported in Table 3 following the September 11, 2001 terrorist attacks indicate that the correlations between Germany and the U.S. increased significantly.

Table 3 Similarly, the correlations between the Japanese and the U.S. markets increased significantly, but decreased (not significantly) going the other way. Increased correlations among major equity markets may reflect the spread of a crisis of confidence within the global investment community. This result implies that events of September 11 may be interpreted as a global shock affecting most of the equity markets in the same direction, thereby giving rise to increased correlations between the U.S. and the Japanese markets and between Germany and the U.S. Summary and Conclusions In investigating the short-term co-movements among the U.S. and German stock markets during 1999 to 2002, our analyses supported the findings of the existing literature that the co-movements among these two markets were significant and varied over time. The Japanese stock market, on the other hand, had almost no significant effect on the movement of the other markets. Despite the significant interdependencies among the markets studied, room for international portfolio diversification nevertheless seems possible. In particular, both German and Japanese investors should consider investing in each others' markets for effective portfolio diversification. Similarly, American investors can realize diversification benefits in Japan. However, diversification benefits are minimal for American and German investors who would like to invest in each others' markets. Lately, investors have been venturing into emerging markets; while there has been an increase in the degree of cyclical co-movement among industrialized countries over time, emerging market economies are not closely correlated with industrial country markets. In fact, ongoing research by the present author confirms that investing in emerging countries offers considerable diversification benefits for international investors. The September 11 terrorist attacks appear to have had the same effect on the relationship of these three markets. Correlations between Japanese and the U.S. markets and the German market and that of the U.S. had both increased. While correlation between German and Japanese markets increased, the change is not statistically significant. These results indicate that correlations do increase following exogenous shocks, a finding that confirms earlier results in the literature. This study demonstrates that it may be possible to reduce the risk associated with stock market investing for a given level of expected returns by diversifying internationally. However, investors must be weary of unexpected events such as the terrorist events of 9/11. Based on the results of this study, increased correlations between international markets indicate that benefits of international diversification diminish after an unexpected exogenous event. It is also important to acknowledge that international investing involves currency risk. The analysis carried out here did not deal with currency risk since fluctuating currency values may reduce or enhance returns. It may be argued that international investing is difficult and not practical for most investors since U.S.-based investors rely primarily on closed-end single country funds and/or international index funds. Further, market indices may not represent easily investible assets due to high costs and entry barriers. However, recent introduction of new products such as exchange traded funds (ETF) have made international investing easer. ETF products track portfolios designed explicitly to allow internationally comparable benchmark performances yet can be easily traded on organized exchanges. Therefore, if foreign stock markets continue to outperform the domestic market along with a favorable economic outlook and easer access, it is likely that foreign markets will continue to be attractive to U.S. investors in the future. ------------------------------------- Burhan F Yavas, PhD, is an adjunct professor, working as a class advisor for Presidential Key Executive (PKE) MBA at the Graziadio School of Business and Management. He is also a professor in accounting and finance at California State University, Dominguez Hills (CSUDH). He consults for corporations and financial institutions in the areas of export-import management, market surveys business forecasting, and corporate strategy. He has lectured and written in a variety of publications, including the Management International Review, Journal of Multinational Financial Management, International Trade Journal, and Journal of Cross Cultural Management. burhan.yavas@pepperdine.edu ------------------------------------- [7] G. Karolyi, R. Stulz. "Why Do Markets Move Together? An Investigation of U.S.-Japan Stock Return Co-movements," Journal of Finance, 51, no. 7, (1996): 951-986. [8] B.F Yavas, F. Rezayat. "Integration among Global Equity Markets: Portfolio Diversification using Exchange Traded Funds," unpublished manuscript.

This article first appeared in Graziadio Business Report, 2007, Vol. 10, Issue 2

|

Management Books worth reading now

|

||||||||||||

|

|

||||||||||||||

| up ñ | back to publications - Management and Strategy | back to themanager.org |

If you have questions or comments to our website, do not hesitate

to contact us (comments and questions are always welcomed):

webmaster2 AT reckliesmp.de

Copyright © 2001 Recklies Management Project GmbH

Status: 01. Juli 2015